M – F / 8:30 – 18:00

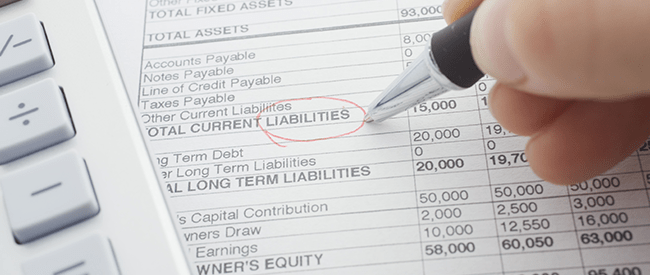

An Annual Balance Sheet is a financial statement that summarizes a company’s assets, liabilities, and shareholders’ equity at a specific point in time. It’s called a balance sheet because the total assets always equal the sum of liabilities and equity. Assets are funded either by borrowing money (liabilities) or by capital invested by shareholders (equity). These three sections help investors understand what the company owns, what it owes, and how much shareholders have invested.

A company balance sheet provides a snapshot of the business’s financial position at the end of the financial year. It shows the accounting value of all assets, liabilities, and equity at that date, helping assess the company’s financial health, including liquidity.

One or more auditors must examine the balance sheet. After auditing, the statements must be submitted to the shareholders for approval at a general meeting within 4 months after the financial year-end. The responsible officer must provide a copy to all shareholders at least 3 days before the meeting and keep copies available at the company office for inspection during the same period. (For public companies, additional disclosure requirements apply, such as publication in a newspaper.)

If the company’s accounts or related documents are lost or damaged, the responsible officer must notify the relevant authority (e.g., the auditor or Accounts Inspector) within 15 days of becoming aware of the loss.

Staying on top of your annual balance sheet is essential for maintaining transparency, meeting legal requirements, and avoiding penalties. Make sure your financial statements are accurately prepared, audited, and submitted on time to the Revenue Department and Department of Business Development.

Contact us today for professional assistance to ensure your company’s annual balance sheet is fully compliant and up to date.

This information is for general guidance only and is not legal, tax, or accounting advice. Requirements may vary depending on your company and circumstances. For professional advice, please consult a licensed lawyer, accountant, or relevant expert.

Licensed CPD in Accountancy

Specialization: Tax Planning, Full Accounting System, Financial Statement

Magna Carta Law Firm website uses cookies. Further details are set out in our Cookies Statement.